Forward commodity markets were created to allow market participants to mitigate price risk for a given commodity. Long before the world ran on oil and natural gas, agricultural commodities traded in the forwards. By the 1860s, the Chicago Board of Trade was using standard instruments to trade wheat, corn, cattle, and pork. By the 1870s, the New York Mercantile Exchange was created by a group of Manhattan dairy merchants looking to standardize the chaotic butter and cheese markets. Over the next 100 years, these markets matured and expanded, but their purpose has remained the same: to create a marketplace that allows buyers and sellers to access a standard and liquid market that mitigates forward risk to commodity price volatility.

Today, futures markets like the NYMEX Henry Hub Natural Gas contracts or the West Texas Intermediate Crude Oil contract are widely referenced and quoted as major benchmarks of energy prices. Other less quoted items like NYISO Zone J contracts are also traded on NYMEX, along with other power market hubs, and on multiple other exchanges like the Intercontinental Exchange (ICE), or even in open-call, over-the-counter markets popular in many power regions. These exchanges give visibility into current market prices for commodities like electricity in NYC for this winter and multiple years into the future.

From a retail power buyer’s perspective, the forward markets allow sellers of retail supply agreements the ability to see where the market is trading. These buyers are able to purchase the underlying wholesale commodity once retail agreements are executed, mitigating their exposure. Buyers can also purchase the commodity on the wholesale market and then sell it in the retail market, hopefully for a profit.

This brief overview offers insights into the tools that market participants use to get clarity on the market’s perceived risk of any commodity. As traders look at the coming winter in New York, they see risks to underlying power markets that have not been observed in over a decade.

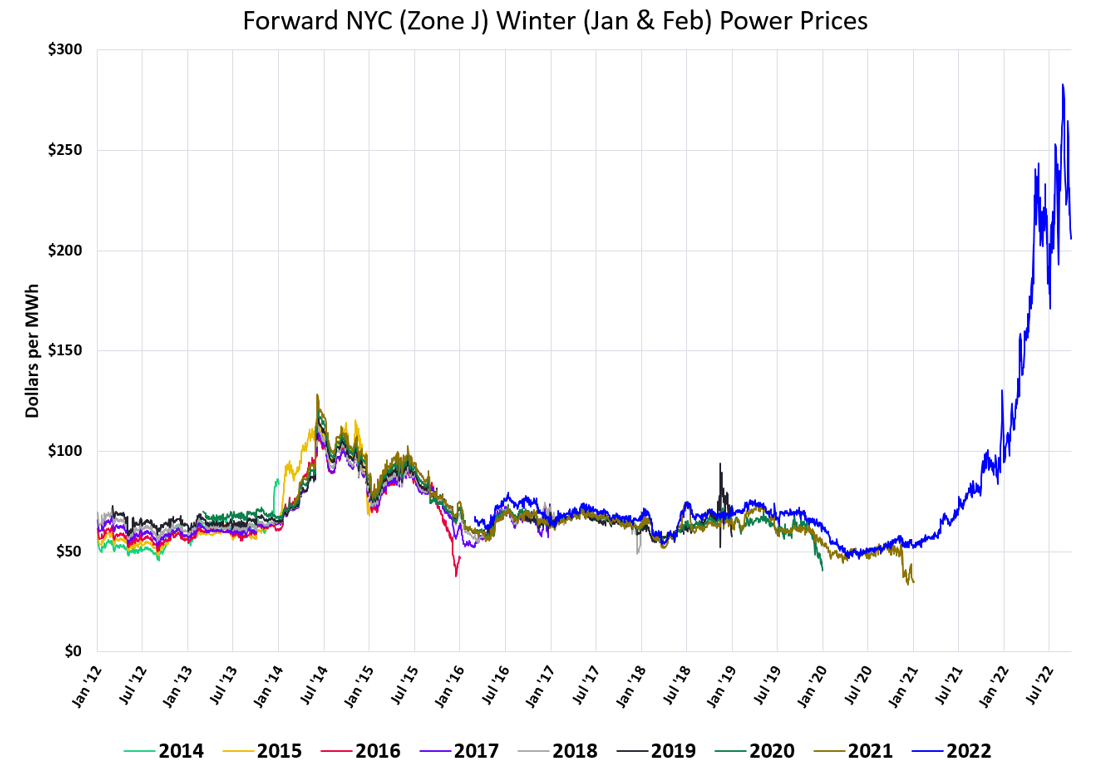

Figure 1 shows the historically traded price in the forward markets for each of the past eight winters compared to the winter of 2022/23 (the months of January and February). This chart clearly suggests that traders expect significantly higher price risk this winter, compared with the past.

Figure 1: Forward NYC (Zone J) Winter (Jan & Feb) Power Prices from 5

Even after the Polar Vortex in the winter of 2014, the following winters of 2015 and beyond never traded above $130 per MWh. At the end of last month, the winter of 2022 was trading just above $280 per MWh, with a fall over the past month down to $205 per MWh. There is not just one driver of this volatility.

Most know that Europe is mired in an energy crisis of unprecedented proportions. Natural gas prices in Europe are trading between $50 and $100 per MMBtu, and power prices are trading as high as $1000 per MWh. What might be news is that those on this side of the Atlantic are not nearly as isolated as anyone previously thought.

In New England, pipeline capacity during the winter months, specifically during the coldest days in winter, is insufficient to meet natural gas demands, which include gas for space heating and for power generation. As the region continues to reduce its dependency on coal and fuel oil, and as nuclear power plants retire, natural gas demand has increased. This lack of adequate pipeline capacity is remedied by the Liquified Natural Gas (LNG) import terminals around Boston Harbor.

The major difference between this winter and winters in the past is that current international LNG prices are near record highs mostly due to the conflict in Europe. This means that the marginal cost of natural gas during the months where traders perceive significant risk of pipeline capacity is set by international LNG prices, and not the price of gas in the Appalachian region. This has led to New England’s power prices for this winter to trade at prices similar to prices in New York City.

Given the fact that the natural gas pipelines and electricity transmission lines between New York and New England are tightly interconnected and dependent on one another, the prices between the two systems are often in parity with one another.

No one can blame Putin for the lack of adequate natural gas pipeline capacity flowing into New England across New York. However, he may have some involvement in withholding natural gas from Europe, which in turn drives up the international price for natural gas. And don’t think that the situation will automatically correct itself once the war in Ukraine is over.

While there are fewer perceived risks for winters beyond this year, each of the next three winters (2024 – 2026) are all trading above historical highs and over $130/MWh. This is mainly due to the belief that even if the war in Ukraine ended tomorrow, European nations are not likely to re-engage with Russia for energy supply in the foreseeable future. This means that future LNG prices for multiple winters to come will likely remain elevated and above $25 per MMBtu at least until 2027.