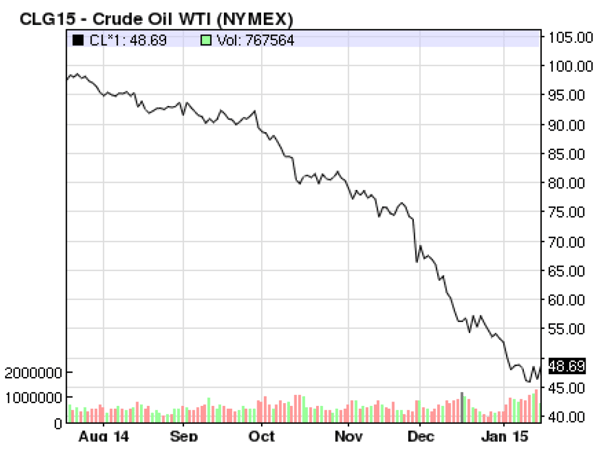

I am pleased to forward 5’s fourth quarter overview of the energy market. Our last letter started with the statement “The speed and scope of changes in the energy market continues to astound us.” The trend continues. Q4 featured a spectacular sell off in crude oil. The price dropped from June highs of $112 per barrel for Brent and $105 per barrel for WTI to $62 per barrel for Brent and $59 per barrel for WTI in December. This sell off continued in January, with crude falling down to almost $45 per barrel. In this issue, we focus on increased volatility in natural gas and power driven, in part, by the drop in oil and natural gas prices in Q4, and two other significant topics, (i) new evidence of the energy market’s fundamental transformation, and (ii) the GOP’s sweeping victory in the November elections.

The Collapse In Oil Prices and The Increase In Volatility

As the following chart demonstrates, it is easy to plot the decline in oil prices. It is much harder to understand what caused this movement.

Commentators have focused on demand and supply issues, but there is no consensus on the degree to which these factors are putting pressure on oil prices. Frequently cited supply side factors include (i) record high Russian output, (ii) an agreement between the Iraqi government and the Kurdish Regional Government on revenue sharing (which can lead to greater exports), (iii) the US shale revolution, and (iv) the Saudi government’s refusal to slow production and cede market share to other producers. Reductions in demand are driven by (i) a weak international economy (China is no longer growing at double digit levels), and (ii) increased fuel efficiency and fuel substitution. In its recent report on oil, Citibank noted that diesel demand has slowed considerably since 2010, falling from double digit growth to negative demand growth in 2014. It is reasonably likely that many, if not all, of these supply and demand factors have contributed to the fall in the price of oil.

Oil’s price does not directly impact electricity and natural gas prices. Oil is a very small input in generation output, constituting approximately 1.5% of the country’s electricity generation in 2011 and 0.7% in 2014. While oil grabbed the headlines, the coincident sell off in natural gas in December was much more important to our clients. In many markets, natural gas drives electricity pricing. After natural gas prices increased in November (due to short term weather), prices dropped in December by the largest amount month over month since July 2008. The selloff in natural gas is easier to explain. On the demand side, November’s cold weather did not return in December. Heating demand was significantly above the 30 year average in November; however it was well below this same average in December. More importantly, production of natural gas continues to surprise to the upside. The U.S. Energy Information Administration (EIA) reported that natural gas production hit an all-time high last October. Improvements to natural gas infrastructure in New England and other North East markets continues to relieve some of the transportation bottlenecks that resulted in high natural gas prices last winter.

Surprisingly, the decline in natural gas prices is not all good news for our clients. Electricity and natural gas prices remain at or near historical lows, and we see limited room for those prices to decline. As natural gas prices decline, the non-fuel portion of a generator’s cost becomes a larger percentage of the cost that the generator must receive in order to operate at a profit. Those somewhat fixed generator operating costs begin to act more and more like a floor as natural gas prices move lower. This is one reason that the recent strong sell off in natural gas did not result in an equivalent reduction in electricity prices. In fact, electricity prices have remained somewhat stable and in some cases (often due to regional factors), even increased.

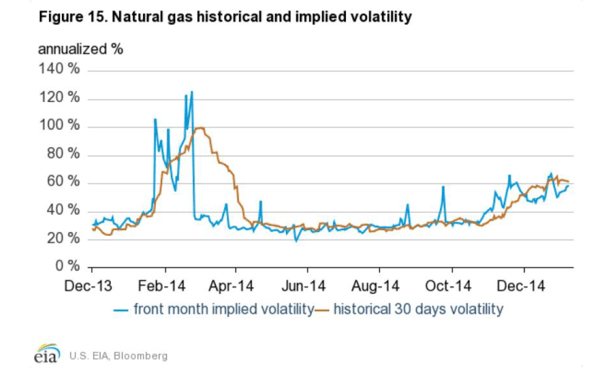

While lower natural gas prices do not always translate into lower electricity prices, they have already resulted in an increase in volatility. In January, the EIA noted this increase in the volatility of natural gas pricing (see below).

This is primarily driven by a market which is now trading at historically low levels. The next event to trigger a price spike may be weather (another polar vortex), political events impacting oil or natural gas supply, reductions in supply, or something else.

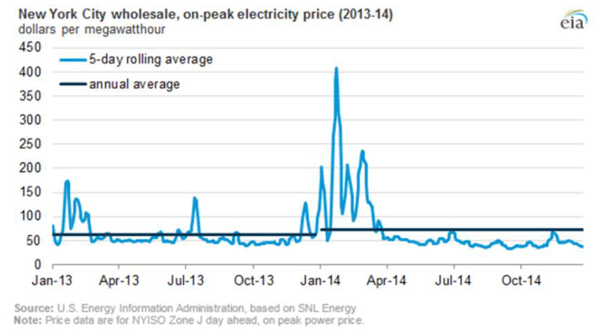

5 is in the risk management business. As we close out 2014, it is worth noting the clear value of taking a structured approach to managing electricity and natural gas exposure (particularly in the Northeast markets). The following chart shows historical pricing in New York City last year.

Consumers that were on a floating price for electricity saw relatively modest pricing for the spring, summer and fall and historically high prices in the winter. Consumers that fixed their price for the entire year paid excess premiums in the spring, summer and fall, and avoided the winter price spikes. The perfect product was neither a fixed price (which would have been at a significant premium to index in the spring, summer and fall) or an index price (which would have exposed the customer to extremely high prices in the winter), but a hybrid. A product that hedged the periods of potential volatility (the winter and summer) and floated at index for the balance of the year. With the recent fall-off in natural gas and oil prices and commensurate increase in volatility, we believe that such a structured approach to price and risk management is also ideal for 2015. The reason for this approach is not just due to changes in the price of natural gas and electricity. As we note in the next section of this letter, fundamental changes in the energy market are accelerating. We have been working with customers since the late 1990s. Throughout this period, each time there have been material changes in the structure of the market, we have seen significant periods of volatility. This is one more reason to approach 2015 with caution.

The Market’s Transformation Accelerates

Last quarter, we commented on several factors pressuring the business model of traditional utilities; increased energy efficiency and new sources of distributed generation reduce demand for existing centralized generation and at the same time, an aging system of pipes and wires requires more investment to maintain. While this puts pressure on incumbent generators and old line utilities, it creates both opportunities and challenges for our clients. Clients must monitor new products and services that can lower costs and generate incremental revenue (such as demand response). At the same time, they need to follow the regulatory efforts likely to result in increased market prices. 5 has expanded its back office team to be sure that we can support our clients across this increasingly broad spectrum of energy related products and services.

The latest developments:

Technology’s impact on the energy market was recognized by the Noble prize committee in Q4. The Nobel Laureates for Physics, Isamu Akasaki, Hiroshi Amano and Shuji Nakamura, received the prize “for the invention of efficient blue light-emitting diodes which has enabled bright and energy-saving white light sources.” Blue light-emitting diodes are the LED lights you now find available for almost all light types. These lights are dramatically longer lasting and more energy efficient. LED lights generate 300 lumens per Watt, which is compared to 16 lumens per Watt for regular light bulbs and 70 lumens per Watt for fluorescents. The lifespan of these lights is equally impressive. LEDs last up to 100,000 hours compared to 1,000 hours for standard bulbs and 10,000 hours for fluorescents.

While efficiency reduces demand, some believe that the most material change agent will be energy storage. A November 2014 article in the law firm Chadbourne & Parke’s newsletter called storage “The Biggest Change to Power Supply Since Edison.” The article noted that combined solar/battery systems are starting to bring the total cost of electricity below the retail price in Germany and Hawaii (markets with very high retail prices) and are expected to become competitive in other states by 2020. The implications for US markets are very exciting. In many states (such as Texas), it is difficult to economically install solar projects because these states have not adopted net-metering. When you have net metering, a facility that generates excess solar power in the summer is credited for that power. Without net metering, a consumer with solar panels loses the benefit of this system when the consumer’s consumption is less than the production of the solar system – significantly reducing the value of the system. Net metering is not needed when a solar system is combined with sufficient energy storage.

In the solar/battery system of the future, the house or business effectively becomes a small utility, generating all of the power it needs from solar panels and using the battery to run the system when there is not sufficient solar generation. Former US Energy Secretary Steven Chu predicts that solar/battery systems will be “as disruptive to electricity distribution and generation as the internet [was to brick-and-mortar businesses].” The Chadbourne article offers an even better analogy – the telecommunications business. “Mobile phones did not replace landlines. Landlines still exist, but mobile phones decentralized telecommunication and dramatically increased the access to and use of telecommunication. Solar-battery systems are about to do the same to power markets.”

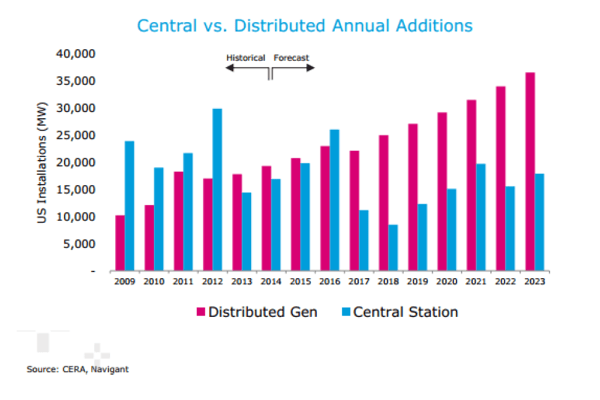

More and more owners of large generation fleets now acknowledge that we are becoming a market where the majority of new generation comes from distributed resources (rooftop solar facilities and other forms of generation generally located on the site of an energy consumer). This is reflected in the following chart:

We do not know if battery storage or new uses of smart meter data will be the primary movers, but we do know that there is an increasingly long list of factors that point to a fundamental transformation of the energy market. Here are a few important points from the last quarter:

- Global investment in clean energy was $310 billion in 2014. Once again China was the leader in renewable energy. China’s investment in clean energy rose 32% to a record $89.5 billion.

- Solar employs more people than coal mining and added 50% more jobs in 2014 than the oil and gas pipeline construction industry and the crude petroleum and natural gas extraction industry combined.

- One out of every 78 new jobs created in the US over the past 12 months was created by the solar industry.

- GE’s wind segment was the fastest growing among GE’s business units in 2014.

- More than 50 million smart meters were installed in 2014. A wide range of new applications were introduced so customers can take advantage of technology.

- For example, a company called Bidgely offer a product, HomeBeat, that now allows the monitoring of home devices without installation of metering equipment.

- 2,200 bills focused on energy efficiency are pending in 50 States.

- Additional innovation is expected in lighting as new companies like Earthtronics and Precision-Paragon introduce more advanced products.

The GOP Takes Control

In November’s national elections, the Republican party scored key victories to gain control of the Senate and extend their majority in the House. The GOP’s control of the both the House and the Senate will make it very difficult for the Obama administration to use legislation to achieve its policy goals. Instead, President Obama will continue to have to lean hard on the EPA and other regulators to push forward the Clean Power Plan (CPP) and other objectives.

The Chair of the Senate Energy and Natural Resources Committee will be Senator Lisa Murkowski (R-AK) and the Chair of the Senate Environment and Public Works Committee will be James Inhofe (R-OK). The latter’s 2012 book on climate change was titled “The Greatest Hoax.” Senator Inhofe will surely make the debate more interesting. The impact of the election is visible in pending legislation to accelerate approval of the Keystone Pipeline. This legislation has been approved by the House and is being debated in the Senate. The new congress is also expected to support those companies looking to export LNG. Bills to expedite the licensing of LNG export facilities were introduced in the Senate on January 6th and in the House on January 14th. We could also see an effort to lift the current ban on crude oil exports.

Notwithstanding Republican control of Congress, we do not expect the election to slow the on-going transformation of the energy market. At this point, there is simply too much money chasing new solutions (both based on renewables and other sources of generation), and most of these solutions are economical with or without a price for carbon. While there is clearly a change in the votes to support climate-change-related policies, it may no longer matter if the Federal Government believes in climate change.

The comparisons to the telecom industry are inevitable. As the Chadbourne article points out, new energy technologies (particularly distributed generation) are to existing generation much as the cell phone was to landlines, and more and more money is betting on the side of this technology. We expect that the EPA will continue to press forward with the Clean Power Plan and its proposed regulations on both existing and new power plants regardless of the change in Congress. While these proposed rules will be the subject of long and complex debates, we think that the EPA will continue to make progress in getting the CPP adopted. Of course, this does not mean that the entrenched interest groups, owners of coal and nuclear generators, and traditional utilities will give up without a fight. There are a range of regulations pending that could benefit these utilities and owners of generation at the cost of energy consumers. These include changes to demand response rules, a new capacity performance plan in PJM, dedicated payments to nuclear operators and many others. We will discuss these and other pending changes in future letters.