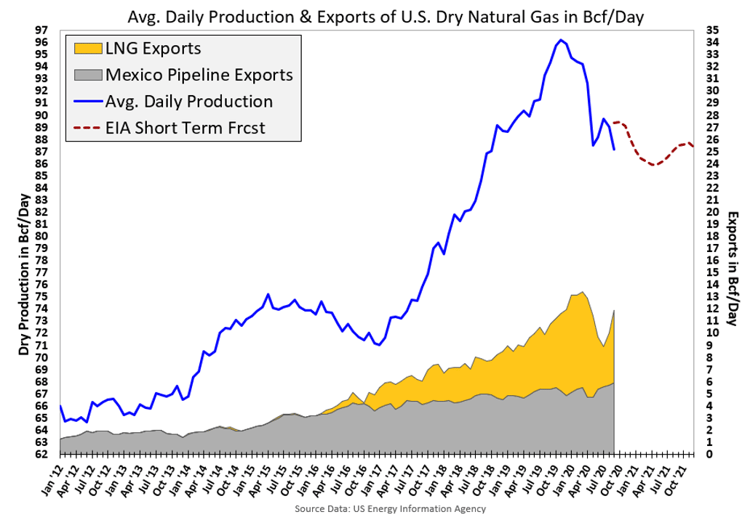

The rise in the futures price for the 2021 NYMEX Henry Hub natural gas contract has been driven by one major fundamental driver - the steady decline in natural gas production over the last 10 months. Figure 1 shows that in November 2019 the EIA reported a record high average daily production of dry natural gas of 96.2 billion cubic feet (Bcf) per day. In September 2020 the daily average production fell to only 87.1 Bcf/day, a decrease of 9.4%. Even with a decline in gas production, the mild winter last year and the demand destruction from coronavirus has created a situation where there will likely be record levels of natural gas in storage.

Figure 1: Avg. Daily Production & Exports of U.S. Dry Natural Gas from eia.gov

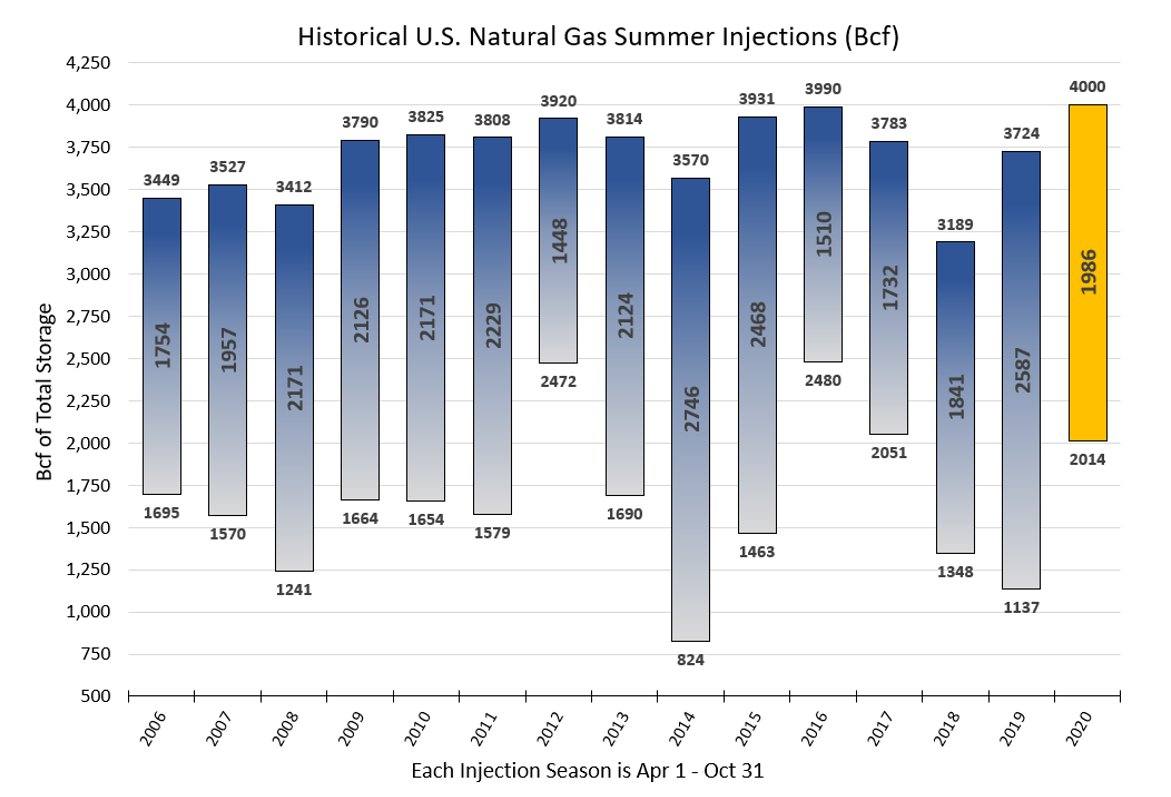

Figure 2 shows the amount of natural gas placed into storage over the last 14 years during injection season (April to October). And while there appears to be plenty of domestic natural gas, traders are concerned that production slow-downs could deplete what is in storage. The EIA’s Short Term Energy Outlook (the red line in Figure 1) shows that production in 2021 should average just under 87 Bcf/day, compared to 91 Bcf/day over the past 12 months. That 4 Bcf/day decrease equates to a deficit of approximately 1,500 Bcf over the course of a year. This is a significant amount of natural gas given that 1,986 Bcf of gas was placed into storage this year. Traders are concerned that storage levels going into the winter of 2021/22 could be down significantly from where they are today.

Figure 2: Historical U.S. Natural Gas Summer Injections from 5

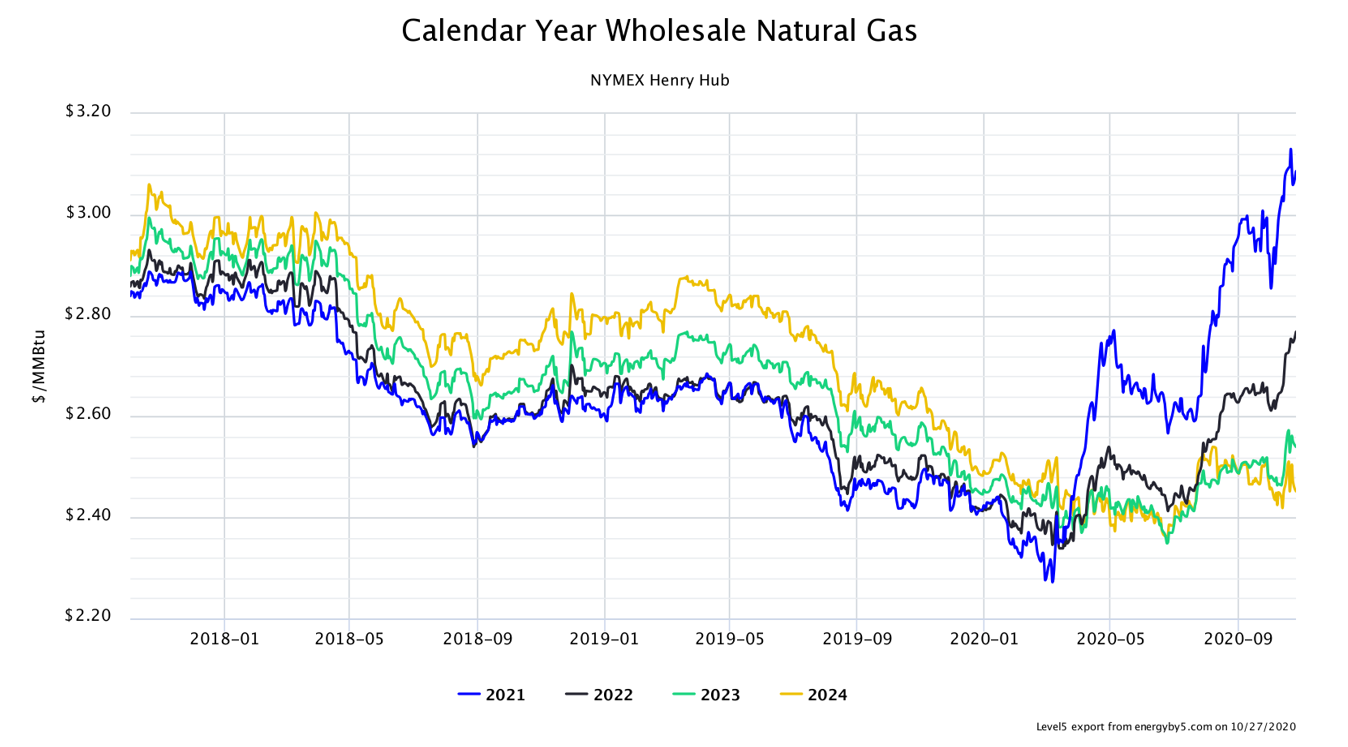

The potential for a much lower storage situation in 2021 has been the fundamental driver behind the rally in gas prices for calendar year 2021 (blue line) as shown in Figure 3. The real question for most buyers of natural gas, who have not hedged their prices for 2021, is “What happens from here? Will prices continue to climb? Have we reached the top? Will prices reverse and come back down off current 36-month highs?" To answer these questions a technical analysis is required which examines how a commodity has been trading and trending as opposed to a fundamental analysis which evaluates the balance of supply and demand.

Figure 3: Calendar Year Wholesale Natural Gas NYMEX Henry Hub from 5

Figure 4 shows how prices for the January 2021 gas contract have traded over the last several months. The red and green bars indicate a decrease and increase, respectively, in futures prices on a given trading day. From a technical point of view, gas prices for January 2021 has seen a steady increase in market prices from late July through early September, and then began to trade within a $0.25 range with the highest point of that range at approximately $3.45/MMBtu. Twice in the last month the market rallied up to $3.45/MMBtu but could not push through that price point and both times retreated from that high.

Figure 4: Henry Hub Natural Gas Futures (Jan 2021) from cmegroup.com

Lately the bottom of the trading range has been approximately $3.20/MMBtu, with only one day where the market was trading around $3.15. The support level (floor) for this market is fairly strong in the $3.15 to $3.20 range, which is about $0.20 below current market prices.

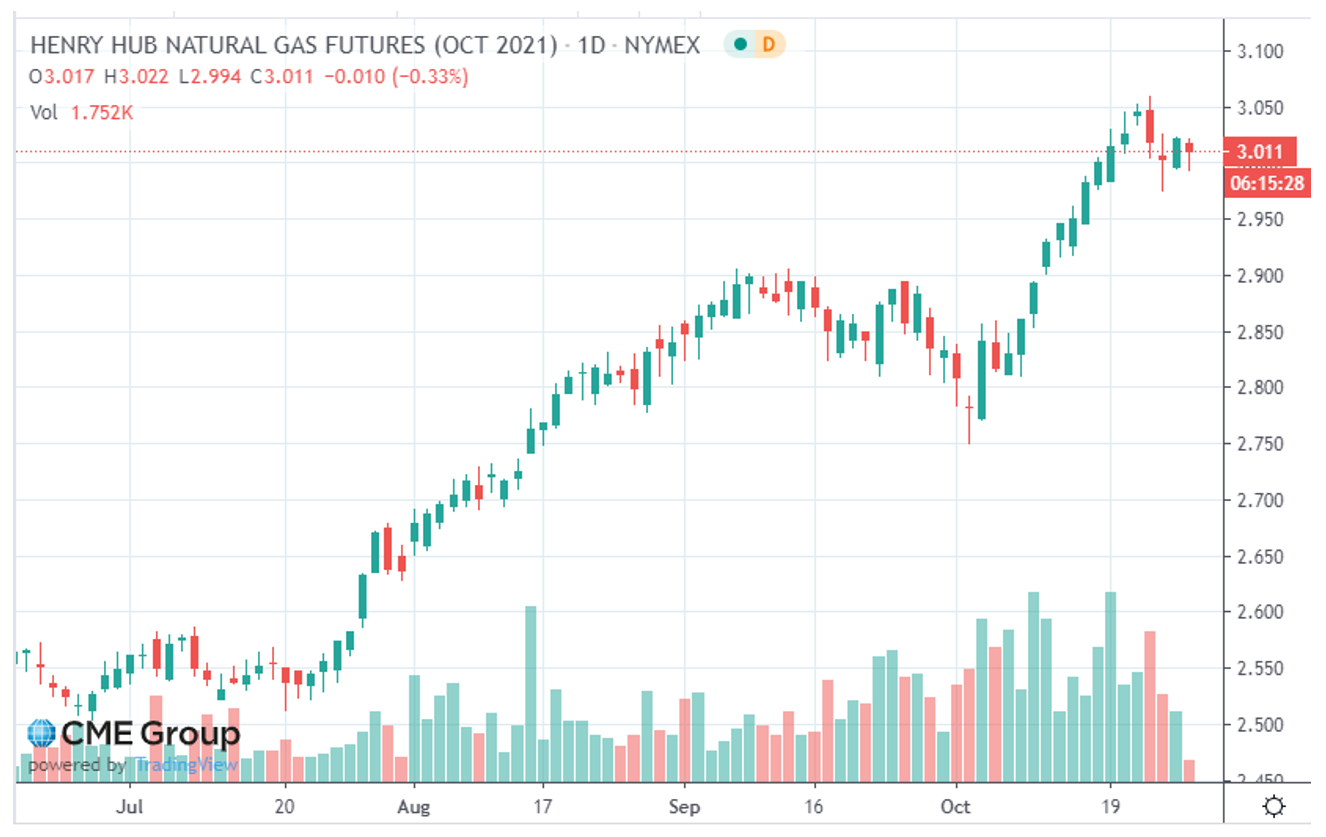

Moving out to the October 2021 gas contract in Figure 5, the resistance levels (ceilings) are not as strong. The market has only bounced off the top price of $3.05/MMBtu once, is still within $0.04 from that high price and seems poised to continue its upward trend.

Figure 5: Henry Hub Natural Gas Futures (Oct 2021) from cmegroup.com

It appears, at least in the short-term, that gas prices for the first six months of 2021 might be slightly bearish (downward trending) and more neutral to slightly bullish (upward trending) for the last half of the year. Beyond the short-term, the severity of this coming winter will have a significant impact on how much prices in the last half of 2021 either continue to rally or fall. The other side of the coin is that a weak winter and depressed spot prices in 2021 will likely push up prices in calendar years 2022 and 2023, as producers see no reason to invest additional capital into a market with weak spot and low futures prices.