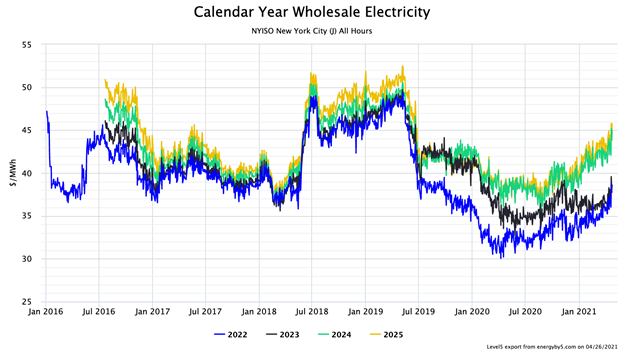

Wholesale electricity prices in New York City have been rising for the last several months. Figure 1 shows how forward prices for calendar years 2022 through 2025 have been trading over the last five years. Note that wholesale prices were at a low at the start of the pandemic in March 2020. Despite a correction in the late fall when the market dropped, the overall trend has been bullish for nearly a year. Additionally, this is a classic example of a contango market, where prices get more expensive with each subsequent time period in the forwards. Figure 1 also shows that the least expensive calendar year is 2022 and that 2025 is the most expensive.

One interesting observation is that the outer years (2024 and 2025) are rising at a similar and faster rate compared to calendar years 2022 and 2023 which seem to have consolidated. We reported on this consolidation in February and suggested that this created good near-term buying opportunities and now 2022 and 2023 are both trading at a $7/MWh (0.7¢/kWh) discount to 2024 and 2025. While the overall market trend in NYC has been bullish, 2022 and 2023 are within $6/MWh (0.6 ¢/kWh) of the 5-year low, which was set immediately before the pandemic. This, coupled with falling capacity prices in NYC, has produced good purchasing opportunities for NYC electricity buyers.

Figure 1: Calendar Year Wholesale Electricity NYISO from 5

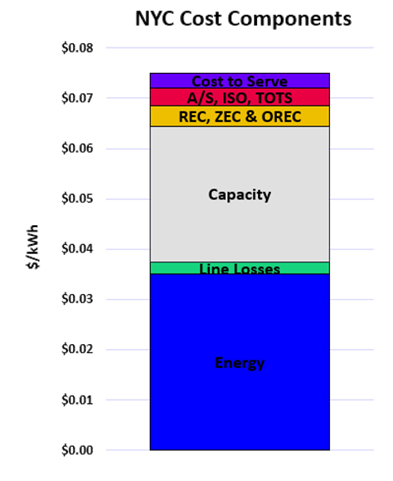

It is easy to assume that rising wholesale electricity prices translate into higher retail electricity prices. However, this is not always true, since energy is only one of several pricing components that make up a retail electricity price. After electricity, the next largest price component is capacity and, fortunately, capacity prices have dramatically fallen in New York City.

Figure 2 shows the cost components of a typical retail electricity offer in New York City. Wholesale energy is shown in blue, and capacity is in gray. For a retail electricity price of 7.5¢/kWh, approximately 3.0¢/kWh is from the cost of capacity. Note that capacity costs are also similar in magnitude to the cost of wholesale energy.

Figure 2: NYC Cost Components from 5

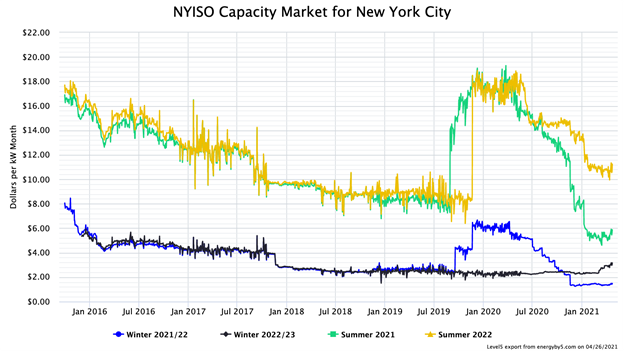

Capacity in New York trades by calendar month, but the prices for these months are established through a winter (Nov-Apr) and summer (May-Oct) auction. Figure 3 shows how capacity for the summer of 2021 through the winter of 2022/23 has been trading in the forward market. This chart shows that the prices of summer capacity in 2021 (green line) and 2022 (yellow line) have fallen by 68% and 40% since January 2020. Additionally, capacity prices for the winter of 2021/22 have also fallen by approximately 80% over that same period. Note that near-term capacity prices, for the summer of 2021 through the winter of 2021/22, are both at their five-year lows.

Figure 3: NYISO Capacity Market for New York City from 5

Recent updates by the New York Independent System Operator (NYISO) are responsible for this dramatic fall in capacity prices. Less electricity demand from the overall economy and more energy efficiency measures have contributed to lower peak usage forecasts. However, the two main drivers are changes to the amount of in-city capacity that must be purchased by retail electricity suppliers and a decrease in this summer’s expected peak load in NYC.

- Less in-city capacity must be purchased: In the previous planning year, retail electricity suppliers were required to purchase 86.6% of its capacity requirements from generating assets within NYC. This requirement was decreased to 80.3% for the current planning year. This means that retail electricity suppliers have to purchase less capacity within Zone J.

- Lower summer peak demand: When this summer’s peak demand forecast in NYC was lowered from 11,477 MWs to 11,199 MWs, the amount of in-city capacity that needed to be purchased was also lowered by 1,000 MWs (11,477 MW x 86.6% = 9,939 MW vs. 11,199 MW x 80.3% = 8,992 MW). In a market like NYC, where generating capacity is limited, this 10% decrease had a material and negative impact on capacity prices in Zone J.

Even though wholesale electricity prices have rallied over the last year, falling capacity prices have produced excellent purchasing opportunities. Clients in NYC with open positions over the next 12 to 18 months should aggressively examine offers for electricity supply. Offers are likely to be at or below current contracted rates, providing significant near-term cost-saving opportunities.